Term Insurance vs Life Insurance Explained: A Complete Beginner’s Guide

Meta Description

Confused between term insurance and life insurance? Learn the key differences, benefits, examples, and how to choose the right policy for your financial security.

Introduction

In today’s uncertain world, financial protection for your family is not just a choice—it is a responsibility. Insurance plays a crucial role in safeguarding your loved ones from unexpected financial burdens. However, many people get confused between term insurance and life insurance.

While both serve the purpose of protection, they work very differently in terms of cost, benefits, and long-term value. This guide will clearly explain the difference so you can make a wise and practical decision.

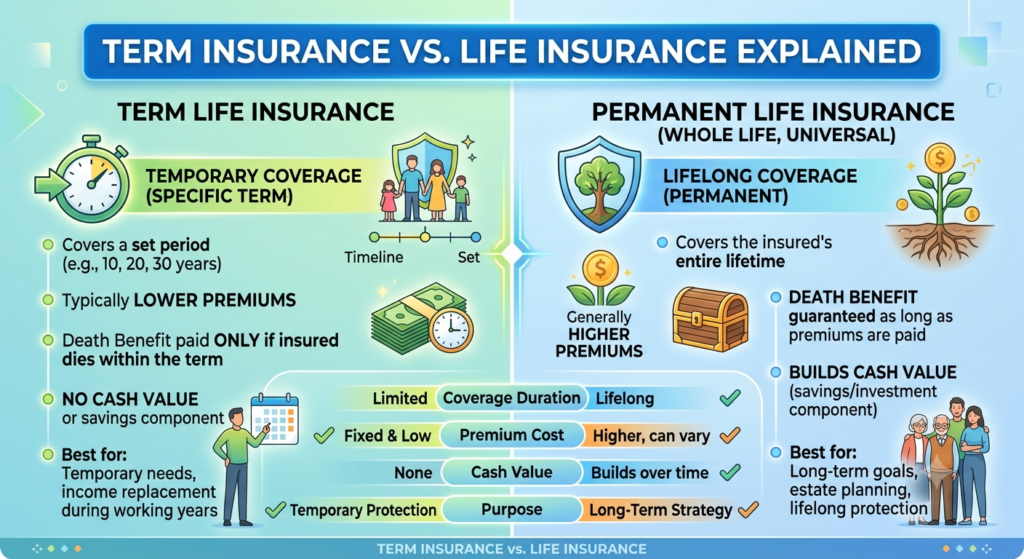

What is Term Insurance?

Term insurance is the simplest and most affordable form of life insurance.

- It provides pure financial protection for a fixed period (term).

- If the policyholder dies during the term, the nominee receives the sum assured.

- If the policyholder survives the term, no maturity benefit is paid (in most plans).

Key Features of Term Insurance

- High coverage at low premium

- Fixed policy duration (10, 20, 30 years, etc.)

- No savings or investment component

- Ideal for income protection

Example

Suppose you take a term plan of ₹1 crore for 25 years by paying ₹10,000 annually.

- If something happens during the term → family gets ₹1 crore

- If you survive → no payout

What is Life Insurance?

Life insurance is a broader category that includes various policies combining protection + savings/investment.

Unlike term insurance, many life insurance plans provide maturity benefits along with insurance coverage.

Types of Life Insurance

- Whole Life Insurance

- Endowment Plans

- Money-Back Plans

- ULIPs (Unit Linked Insurance Plans)

Key Features of Life Insurance

- Provides life cover + savings

- Offers maturity benefits

- Premiums are higher compared to term plans

- Suitable for long-term financial goals

Example

You invest ₹50,000 annually in a life insurance policy for 20 years.

- If you survive → you receive maturity amount (say ₹12–15 lakh)

- If death occurs → nominee gets insured amount

Term Insurance vs Life Insurance: Key Differences

1. Purpose

- Term Insurance: Pure protection

- Life Insurance: Protection + savings/investment

2. Premium Cost

- Term Insurance: Very low

- Life Insurance: Higher premiums

3. Maturity Benefit

- Term Insurance: Usually none

- Life Insurance: Yes, maturity payout available

4. Coverage Amount

- Term Insurance: High coverage (₹1 crore+ easily affordable)

- Life Insurance: Lower coverage for same premium

5. Simplicity

- Term Insurance: Simple and easy to understand

- Life Insurance: Complex due to investment component

6. Returns

- Term Insurance: No returns (pure risk cover)

- Life Insurance: Offers returns (but usually lower than mutual funds)

Advantages of Term Insurance

- Affordable for everyone

- High financial protection

- Ideal for breadwinners

- Peace of mind for family security

- Simple and transparent

Who Should Choose Term Insurance?

- Young professionals

- People with dependents

- Those with loans (home loan, personal loan)

- Anyone seeking maximum coverage at low cost

Advantages of Life Insurance

- Combines insurance and savings

- Helps in disciplined long-term investment

- Provides maturity benefit

- Useful for wealth planning

Who Should Choose Life Insurance?

- People who want forced savings

- Those planning long-term goals (marriage, retirement)

- Risk-averse investors

Real-Life Comparison Example

Let’s compare two individuals:

Person A – Term Insurance

- Premium: ₹12,000/year

- Coverage: ₹1 crore

- Term: 30 years

Person B – Life Insurance

- Premium: ₹50,000/year

- Coverage: ₹10–15 lakh

- Maturity: ₹12–18 lakh

Observation

- Person A gets higher protection

- Person B gets lower protection but savings

This shows that term insurance is better for security, while life insurance is suitable for combined goals.

Which One is Better?

There is no one-size-fits-all answer.

Choose Term Insurance if:

- Your priority is family protection

- You want maximum coverage at low cost

- You are comfortable investing separately (SIP, mutual funds)

Choose Life Insurance if:

- You prefer guaranteed savings

- You want discipline in investment

- You are not interested in market-linked investments

Smart Strategy (Best Approach)

A balanced and traditional wisdom-based approach is:

👉 Take Term Insurance + Invest Separately

- Buy a term plan for protection

- Invest in SIPs or other instruments for wealth

This gives you:

- High protection

- Better returns

- Financial flexibility

Common Mistakes to Avoid

- Buying insurance only for tax saving

- Mixing insurance with investment blindly

- Choosing low coverage

- Ignoring inflation

- Delaying insurance purchase

FAQs

1. Is term insurance better than life insurance?

Yes, for pure protection, term insurance is better due to low cost and high coverage.

2. Can I get money back in term insurance?

Generally no, but some plans offer return of premium (higher cost).

3. Why is term insurance cheaper?

Because it provides only risk coverage, without savings or investment.

4. Is life insurance a good investment?

It is safe but gives lower returns compared to mutual funds or stocks.

5. At what age should I buy insurance?

As early as possible. Premiums are lower when you are young.

Conclusion

Understanding the difference between term insurance and life insurance is essential for building a strong financial foundation. Term insurance offers unmatched protection at a low cost, while life insurance provides a mix of security and savings.

A wise individual does not rely on a single option but chooses a balanced path—protecting family through term insurance and growing wealth through disciplined investments.

Start early, choose wisely, and secure not just your future, but the future of those who depend on you.

Read on Mutual Funds & SIP